Rule 3901-3-07 | Credit for life reinsurance agreements.

(A) Scope

This rule shall apply to all domestic life insurers and to all other licensed life insurers which are not subject to a substantially similar regulation in their state of domicile. This rule shall also apply to all domestic property and casualty insurers with respect to their accident and health business and to all other licensed property and casualty insurers with respect to their accident and health business which are not subject to a substantially similar regulation in their state of domicile. This rule shall not apply to assumption reinsurance, yearly renewable term reinsurance or certain nonproportional reinsurance such as stop loss or catastrophe reinsurance.

(B) Purpose

The purpose of this rule is to facilitate the department's surveillance of the financial condition of insurers by establishing accounting requirements for insurers to reduce any liability or establish any asset in any financial statement filed with the department based on reinsurance ceded by the insurer. These requirements are to ensure that financial statements accurately reflect the financial condition of a ceding insurer, and that a ceding insurer has not reduced liabilities or established assets through the improper use of reinsurance reserve credits.

(C) Authority

This rule is issued under the authority vested in the superintendent under sections 3901.041, 3901.62 and 3901.77 of the Revised Code.

(D) Accounting requirements

(1) No insurer subject to this rule shall, for reinsurance ceded, reduce any liability or establish any asset in any financial statement filed with the department if, by the terms of the reinsurance agreement, in substance or effect, any of the following conditions exist:

(a) Renewal expense allowance provided or to be provided to the ceding insurer by the reinsurer in any accounting period, are not sufficient to cover anticipated allocable renewal expenses of the ceding insurer on the portion of the business reinsured, unless a liability is established for the present value of the shortfall (using assumptions equal to the applicable statutory reserve basis on the business reinsured). Those expenses include commissions, premium taxes and direct expenses including, but not limited to, billing, valuation, claims and maintenance expected by the company at the time the business is reinsured;

(b) The ceding insurer can be deprived of surplus or assets at the reinsurer's option or automatically upon the occurrence of some event, such as the insolvency of the ceding insurer, except that termination of the reinsurance agreement by the reinsurer for nonpayment of reinsurance premiums or other amounts due, such as modified coinsurance reserve adjustments, interest and adjustments on funds withheld, and tax reimbursements, shall not be considered to be such a deprivation of surplus or assets;

(c) The ceding insurer is required to reimburse the reinsurer for negative experience under the reinsurance agreement, except that neither offsetting experience refunds against current and prior years' losses under the agreement nor payment by the ceding insurer of an amount equal to the current and prior years' losses under the agreement upon voluntary termination of in force reinsurance by the ceding insurer shall be considered such a reimbursement to the reinsurer for negative experience. Voluntary termination does not include situations where termination occurs because of unreasonable provisions which allow the reinsurer to reduce its risk under the agreement. An example of such a provision is the right of the reinsurer to increase reinsurance premiums or risk and expense charges to excessive levels forcing the ceding company to prematurely terminate the reinsurance treaty;

(d) The ceding insurer must, at specific points in time scheduled in the agreement, terminate or automatically recapture all or part of the reinsurance ceded;

(e) The reinsurance agreement involves the possible payment by the ceding insurer to the reinsurer of amounts other than from income realized from the reinsured policies. For example, it is improper for a ceding company to pay reinsurance premiums, or other fees or charges to a reinsurer which are greater than the direct premiums collected by the ceding company;

(f) The treaty does not transfer all of the significant risk inherent in the business being reinsured. The following table identifies for a representative sampling of products or type of business, the risks which are considered to be significant. For products not specifically included, the risks determined to be significant shall be consistent with this table.

Risk categories:

(i) Morbidity

(ii) Mortality

(iii) Lapse

This is the risk that a policy will voluntarily terminate prior to the recoupment of a statutory surplus strain experienced at issuance of the policy.

(iv) Credit quality (C1)

This is the risk that invested assets supporting the reinsured business will decrease in value. The main hazards are that assets will default or that there will be a decrease in earning power. It excludes market value declines due to changes in interest rate.

(v) Reinvestment (C3)

This is the risk that interest rates will fall and funds reinvested (coupon payments or monies received upon asset maturity or call) will therefore earn less than expected. If asset durations are less than liability durations, the mismatch will increase.

(vi) Disintermediation (C3)

This is the risk that interest rates rise and policy loans and surrenders increase or maturing contracts do not renew at anticipated rates of renewal. If asset durations are greater than the liability durations, the mismatch will increase. Policyholders will move their funds into new products offering higher rates. The company may have to sell assets at a loss to provide for these withdrawals.

| + - significant 0 - insignificant | ||||||

| RISK CATEGORY | ||||||

| a | b | c | d | e | f | |

| Health insurance - other thanLTC/LTD* | + | 0 | + | 0 | 0 | 0 |

| Health insurance - LTC/LTD* | + | 0 | + | + | + | 0 |

| Immediate annuities | 0 | + | 0 | + | + | 0 |

| Single premium deferred annuities | 0 | 0 | + | + | + | + |

| Flexible premium deferred annuities | 0 | 0 | + | + | + | + |

| Guaranteed interest contracts | 0 | 0 | 0 | + | + | + |

| Other annuity deposit business | 0 | 0 | + | + | + | + |

| Single premium whole life | 0 | + | + | + | + | + |

| Traditional non-par permanent | 0 | + | + | + | + | + |

| Traditional non-par term | 0 | + | + | 0 | 0 | 0 |

| Traditional par permanent | 0 | + | + | + | + | + |

| Traditional par term | 0 | + | + | 0 | 0 | 0 |

| Adjustable premium permanent | 0 | + | + | + | + | + |

| Indeterminate premium permanent | 0 | + | + | + | + | + |

| Universal life flexible premium | 0 | + | + | + | + | + |

| Universal life fixed premium | 0 | + | + | + | + | + |

| Universal life fixed premium | 0 | + | + | + | + | + |

| Dump-in premiums allowed | ||||||

| *LTC = long term care insurance | ||||||

| LTD = long term disability insurance |

(g)

(i) The credit quality, reinvestment, or disintermediation risk is significant for the business reinsured and the ceding company does not (other than for the classes of business excepted in paragraph (D)(1)(g)(ii) of this rule either transfer the underlying assets to the reinsurer or legally segregate such assets in a trust or escrow account or otherwise establish a mechanism satisfactory to the superintendent which legally segregates, by contract or contract provision, the underlying assets.

(ii) Notwithstanding the requirements of paragraph (D)(1)(g)(i) of this rule, the assets supporting the reserves for the following classes of business and any classes of business which do not have a significant credit quality, reinvestment or disintermediation risk may be held by the ceding company without segregation of such assets:

(a) Health insurance - LTC/LTD

(b) Traditional non-par permanent

(c) Traditional par permanent

(d) Adjustable premium permanent

(e) Indeterminate premium permanent

(f) Universal life fixed premium (no dump-in premiums allowed)

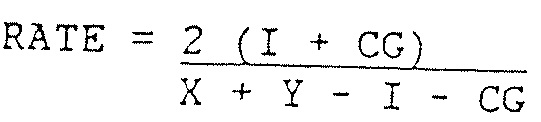

The associated formula for determining the reserve interest rate adjustment must use a formula which reflects the ceding company's investment earnings and incorporates all realized and unrealized gains and losses reflected in the statutory statement. The following is an acceptable formula:

Where: I is the net investment income

CG is capital gains less capital losses

X is the current year cash and invested assets plus investment income due and accrued less borrowed money

Y is the same as X but for the prior year

(h) Settlements are made less frequently than quarterly or payments due from the reinsurer are not made in cash within ninety days of the settlement date.

(i) The ceding insurer is required to make representations or warranties not reasonably related to the business being reinsured.

(j) The ceding insurer is required to make representations or warranties about future performance of the business being reinsured.

(k) The reinsurance agreement is entered into for the principal purpose of producing significant surplus aid for the ceding insurer, typically on a temporary basis, while not transferring all of the significant risks inherent in the business reinsured and, in substance or effect, the expected potential liability to the ceding insurer remains basically unchanged.

(2) Notwithstanding paragraph (D)(1) of this rule, an insurer subject to this rule may, with the prior approval of the superintendent take such reserve credit as the superintendent may deem consistent with the insurance law, rules and regulations, including actuarial interpretations or standards adopted by the department.

(3)

(a) Agreements entered into after the effective date of this regulation which involve the reinsurance of business issued prior to the effective date of the agreements, along with any subsequent amendments thereto, shall be filed by the ceding company with the commissioner within thirty days from its date of execution. Each filing shall include data detailing the financial impact of the transaction. The ceding insurer's actuary who signs the financial statement actuarial opinion with respect to valuation of reserves shall consider this rule and any applicable actuarial standards of practice when determining the proper credit in financial statements filed with this department. The actuary should maintain adequate documentation and be prepared upon request to describe the actuarial work performed for inclusion in the financial statements and to demonstrate that such work conforms to this rule.

(b) Any increase in surplus net of federal income tax resulting from arrangements described in paragraph (D)(3)(a) of this rule shall be identified separately on the insurer's statutory financial statement as a surplus item (aggregate write-ins for gains and losses in surplus in the capital and surplus account, page four of the annual statement) and recognition of the surplus increase as income shall be reflected on a net of tax basis in the "Reinsurance ceded" line, page four of the annual statement as earnings emerge from the business reinsured.

{For example, on the last day of calendar year N, company XYZ pays a $20 million initial commission and expense allowance to company ABC for reinsuring an existing block of business. Assuming a thirty-four per cent tax rate, the net increase in surplus at inception is $13.2 million ($20 million - $6.8 million) which is reported on the "Aggregate write-ins for gains and losses in surplus" line in the capital and surplus account. $6.8 million (thirty-four percent of $20 million) is reported as income on the "Commissions and expense allowances on reinsurance ceded" line of the summary of operations.

At the end of year N + 1 the business has earned $4 million. ABC has paid $.5 million in profit and risk charges in arrears for the year and has received a $1 million experience refund. Company ABC's annual statement would report $1.65 million (sixty-six percent of ($4 million - $1 million - $.5 million) up to a maximum of $13.2 million) on the "Commissions and expense allowance on reinsurance ceded" line of the summary of operations, and -$1.65 million on the "Aggregate write-ins for gains and losses in surplus" line of the capital and surplus account. The experience refund would be reported separately as a miscellaneous income item in the summary of operations.}

(E) Written agreements

(1) No reinsurance agreement or amendment to any agreement may be used to reduce any liability or to establish any asset in any financial statement filed with the department, unless the agreement, amendment or a letter of intent has been duly executed by both parties no later than the "as of date" of the financial statement.

(2) In the case of a letter of intent, a reinsurance agreement or an amendment to a reinsurance agreement must be executed within a reasonable period of time, not exceeding ninety days from the execution date of the letter of intent, in order for credit to be granted for the reinsurance ceded.

(F) Existing agreements

Insurers subject to this regulation shall reduce to zero by December 31, 1997 any reserve credits or assets established with respect to reinsurance agreements entered into prior to the effective date of this rule which, under the provisions of this regulation would not be entitled to recognition of the reserve credits or assets; provided, however, that the reinsurance agreements shall have been in compliance with laws or rules in existence immediately preceding the effective date of this rule.

(G) Severability

If any section, term, or paragraph of this rule is adjudged invalid for any reason, such judgment shall not affect, impair or invalidate any other section, term or paragraph of this rule, but the remaining section, terms and paragraph shall be and continue in full force and effect.

Last updated October 11, 2023 at 1:51 PM

Supplemental Information